{"componentChunkName":"component---src-templates-blogpost-tsx","path":"/blog/the-platform-business-taxation-debacle","result":{"pageContext":{"isCreatedByStatefulCreatePages":false,"id":"456c76a2-3096-53d3-8e57-9a39544ac571","title":"The platform business taxation debacle","slug":"the-platform-business-taxation-debacle","published":"2018-06-07T00:00:00.000Z","author":"Dan Whale","content":"### Want your platform business to be prepared for the future? Communicating your users’ tax obligations to them is a start, but innovation exists to go far further.\n\nBusinesses such as online marketplaces or gig/sharing economy platforms, known as ‘platform businesses’, have done rather well in the past few years. Investment has poured in, markets have been dominated and the UK’s most recent [budgets](http://www.sharingeconomyuk.com/news-and-views/post.php?s=2017-11-23-sharing-economy-uk-budget2017-blog) have included provisions for their continued development.\n\nHowever, a recent report revealed that HMRC is still struggling with the taxation of the users of these platforms. The main challenge is not deciding how to apply tax to those making money, but educating them as to what their responsibilities are. HMRC’s March [‘call for evidence’](https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/687363/The_role_of_online_platforms_in_ensuring_tax_compliance_by_their_users.pdf) found that “a quarter of those operating in the sharing economy through online platforms are not confident about their knowledge of tax obligations” with 54% seeing their sharing economy activity as “just a way of making some extra money rather than employment or self-employment.”\n\nThe government has set out to simplify taxation, as it seeks to [“help the UK become leaders of the digital and sharing economy”](https://www.gov.uk/government/publications/income-tax-new-tax-allowance-for-property-and-trading-income/income-tax-new-tax-allowance-for-property-and-trading-income). However, it is also wary that as platform businesses grow, so too does the possibility of people hiding second incomes. Furthermore, the government does not want to lose out on VAT from companies that operate within the UK but are based elsewhere. It has implemented measures to prevent this, such as commitments to collaborative working arrangements, data exchanges and timeliness of responses as evidence of non-compliance.\n\nThe call for evidence also notes that many people making money in this way have never before had to interact with HMRC, as they have always had an employer to act as an intermediary. HMRC is therefore interested in the role platform businesses could play in educating their users on their tax responsibilities.\n\n#### When do your users pay tax?\nBut if, as a platform, businesses are to play a role in displaying a user’s tax obligations, the question naturally presents itself - when do users pay tax? Unfortunately, there is no blanket answer to this question. When your users pay tax will depend on both your and their type of business. That being said, HMRC have recently put a spotlight on platform businesses. “You may need to pay tax if you use websites and apps to sell services like:\n\n * • renting out your home to tourists\n * • renting out your business premises, home or any other property for business purposes\n * • doing tasks, eg cleaning or odd jobs\n * • renting out your personal equipment, eg power tools\n\n\nThis may not be your main job or business. Selling services online like this is sometimes called the ‘sharing economy’ or ‘peer-to-peer’ (P2P) business.”\nIt offers further detail in that as an individual they need to pay tax on selling goods and services online if “income is more than the tax-free allowances and reliefs they’re eligible for.” A simple way to break it down is as follows:\n\n * • If a user gains their income solely from your platform business, they only begin paying tax when their income reaches £11,850 per annum, as is shown in the table below.\n * • If a user has other sources of income but their yearly income from platform businesses is less than £1000, they are unlikely to have to pay tax on it due to the [tax-free allowance on trading and property](https://www.gov.uk/guidance/tax-free-allowances-on-property-and-trading-income).\n * • Those earning over £11,850 from other sources and earning over £1000 from platform businesses, must pay tax on their platform earnings at the rate shown in the table below. This must be done via a self-assessment to HMRC at the end of the tax year.\n\n\n | Band | Taxable Income | Tax Rate |\n | ----------- | ----------- | ----------- |\n | Personal Allowance | Up to £11,850 | 0% |\n | Basic Rate | £11,850 to £46,350 | 20% |\n | Higher Rate | £46,350 to £150,000 | 40% |\n | Additional Rate | Over £150,000 | 45% |\n\nWhat makes things slightly more difficult for online marketplaces is that users may also need to register for VAT. As aforementioned, HMRC’s main VAT concerns have been regarding overseas businesses, but this is not to say that obligations do not fall on UK platforms. Its March report highlights that “Budget 2016 and Autumn Budget 2017 included measures to make online marketplaces jointly and severally liable for the VAT of non-compliant overseas businesses in certain circumstances.” As for UK users, they must register for VAT when VAT taxable turnover (the total of everything sold that is not [excluded from VAT](https://www.gov.uk/guidance/vat-exemption-and-partial-exemption)) goes above the ‘threshold’ of [£85,000](https://www.gov.uk/vat-registration/when-to-register) per annum. \n\nSo where does this leave your business? The key takeaway is this: HMRC knows more needs to be done to tackle this taxation debacle, but it realises that it does not yet have the answers. It has explored how taxation works for the sharing economy in France and Estonia to see if similar models can be applied to the UK, and is now encouraging businesses to contribute ideas to help shape a solution. Principally, it appreciates that “certain businesses are already taking steps to support their users in understanding their tax obligations”, noting that, “This is positive.” However, how this ‘platform-to-user taxation communication’ should manifest itself is still completely unknown.\n\n#### Solutions\nThe immediate solution to this is to follow firms setting a ‘positive’ example and begin communicating tax obligations to users via your platform. This could be done in a manner of ways, including clear diagrams on your website or app, sending tax reminder emails to your users or perhaps running a social media campaign to inform them on their tax requirements.\n\nHowever, there are issues with this approach. Platform businesses are concerned that providing such information would make them liable for its content and the ability of users to understand and implement that information. If a user was found to be evading tax, they could blame the communication of the platform.\n\nIt would be far more beneficial if the information was provided by HMRC itself. This would put platform businesses at ease with what they’re communicating and encourage a close relationship between themselves and HMRC. \n\nWhilst an unquestionably strong step forward, it still does not help users actually pay their tax. As a solution it is little more than an extra post buried in the FAQs of a website which can easily be ignored. A more holistic solution would combine the information with a way for users to meet their tax obligations.\n\n#### Enter Paybase.\nBy partnering with Paybase, you could offer your users a tool to manage their tax themselves. Paybase’s custom built Logic Engine can - with the right input - deduct any amount from a user’s sales and store it in a separate account. Therefore once a user has established their tax obligations, they can configure their own logic to ensure they are saving correctly (e.g. charge me 40% once sales exceed £1000 within a calendar year, or charge me 20% once sales have exceeded £11,850). Whilst it would not send the money directly to HMRC, it would safeguard the money for each user so that they knew they were meeting their obligations.\n\nTo be clear, Paybase would only act as a saving tool, the duty of educating users about their tax requirements would remain with the platform business and/or HMRC. But providing such a useful tool to meet those requirements is a substantial competitive advantage. Considering the competition many platform businesses face in both acquiring and retaining sellers, this customer-centric feature could be exactly what is needed to instil loyalty. Furthermore, it demonstrates a genuine commitment from the platform business to preventing and reducing tax evasion on its platform. As illustrated in the [Criminal Finances Act](http://www.legislation.gov.uk/ukpga/2017/22/part/3/enacted), becoming a platform which tolerates tax evasion is likely to see your business face a far worse punishment than some negative PR.\n\nPublishing HMRC-backed taxation guidelines on your website/app is likely to be the norm within the next few years, so it makes sense to start investigating your users’ tax requirements now - the HMRC helpline can be found [here](https://www.gov.uk/government/organisations/hm-revenue-customs/contact/income-tax-enquiries-for-individuals-pensioners-and-employees). However, partnering with Paybase allows your platform to go that step further in helping users pay the right tax. It is something both they and HMRC need help with - why not lead the way? \n\n\n[Twitter](https://twitter.com/paybase) [LinkedIn](https://www.linkedin.com/company/paybase/)\n","excerpt":"Want your platform business to be prepared for the future? Communicating your users’ tax obligations to them is a start, but innovation exists to go far further.\n\nBusinesses such as online marketplaces or gig/sharing economy platforms, known as ‘plat...","cover":{"src":"https://paybase.imgix.net/blog/The-platform-business-taxation-debacle.jpg","alt":"need one"},"link":{"to":"/blog/the-platform-business-taxation-debacle","copy":"Read more"},"tags":["Platform Economy","Tax","Payments"],"related":[{"id":"e0e81a59-f7c2-517a-b3e0-6c972b0f13af","title":"How do payments work for online marketplaces / gig / sharing economy platforms?","slug":"how-do-payments-work-for-online-marketplaces","published":"2019-02-27T00:00:00.000Z","author":"Dan Whale","content":"\n### Choosing the right payments option can be the best early decision your business makes\n\nIf you are currently setting up your platform and are starting to think about payments, bear in mind, platform payments work differently than payments for more traditional ecommerce businesses.\n\nFor traditional ecommerce businesses, the payment flow is simple. Money is transferred from a buyer to a seller using a payment gateway and acquirer. We won’t walk you through the entire ‘four-party model’ (as it is known) now, but if you’re interested in how it works, [this article](https://www.visaeurope.com/about-us/four-party-model/) explains it well. This is how online card payments have been made for decades, with the experience becoming sleeker and quicker for the customer in recent years.\n\nBut the payment flow of a platform business is different. Platform businesses do not usually sell their own products or services. Instead, they connect buyers and sellers and charge a commission on transactions between them. This means that payments need to be routed. This can be done in one of two ways.\n\nThe first method is to use a payment gateway and acquirer as traditional ecommerce businesses do. This entails taking in all payments from your buyers centrally, then calculating your commission, before finally manually transferring the remainder to each individual seller.\n\n

\n \n

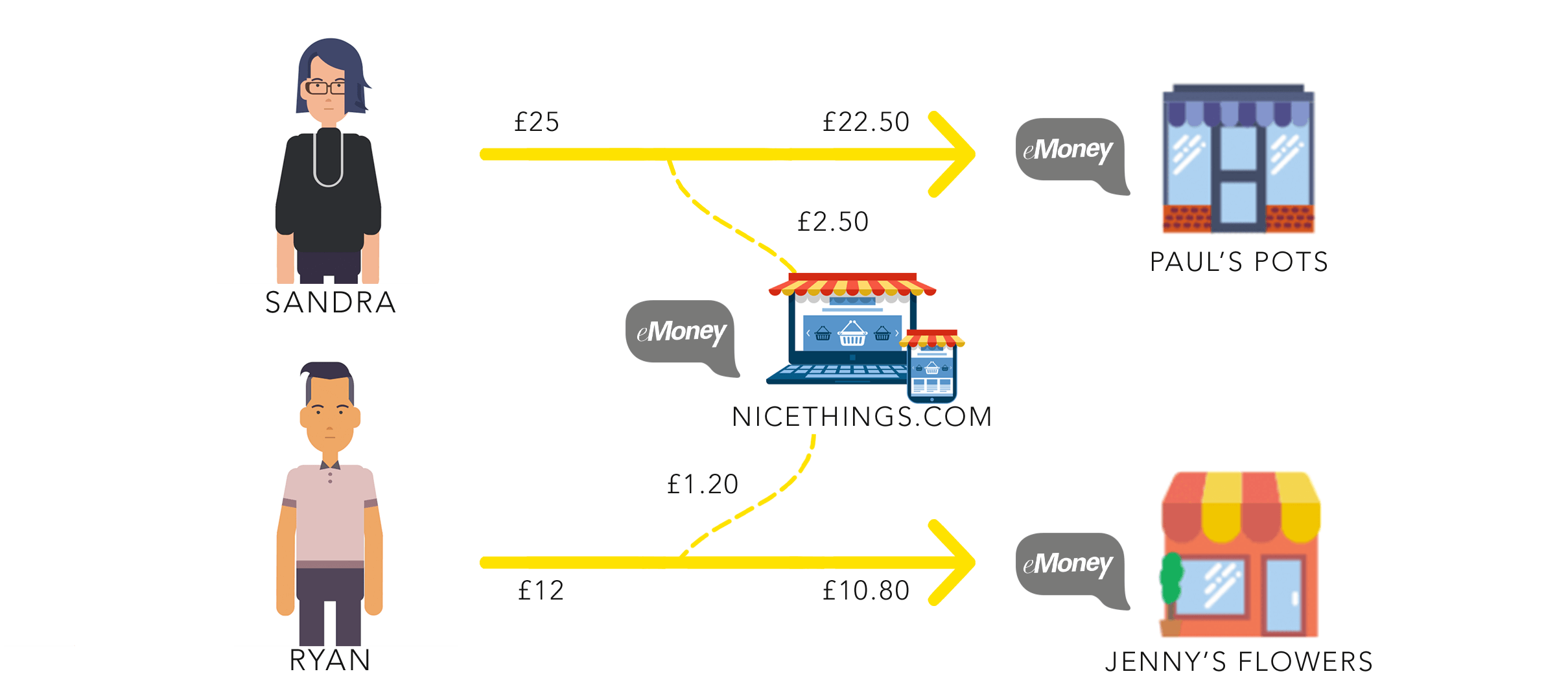

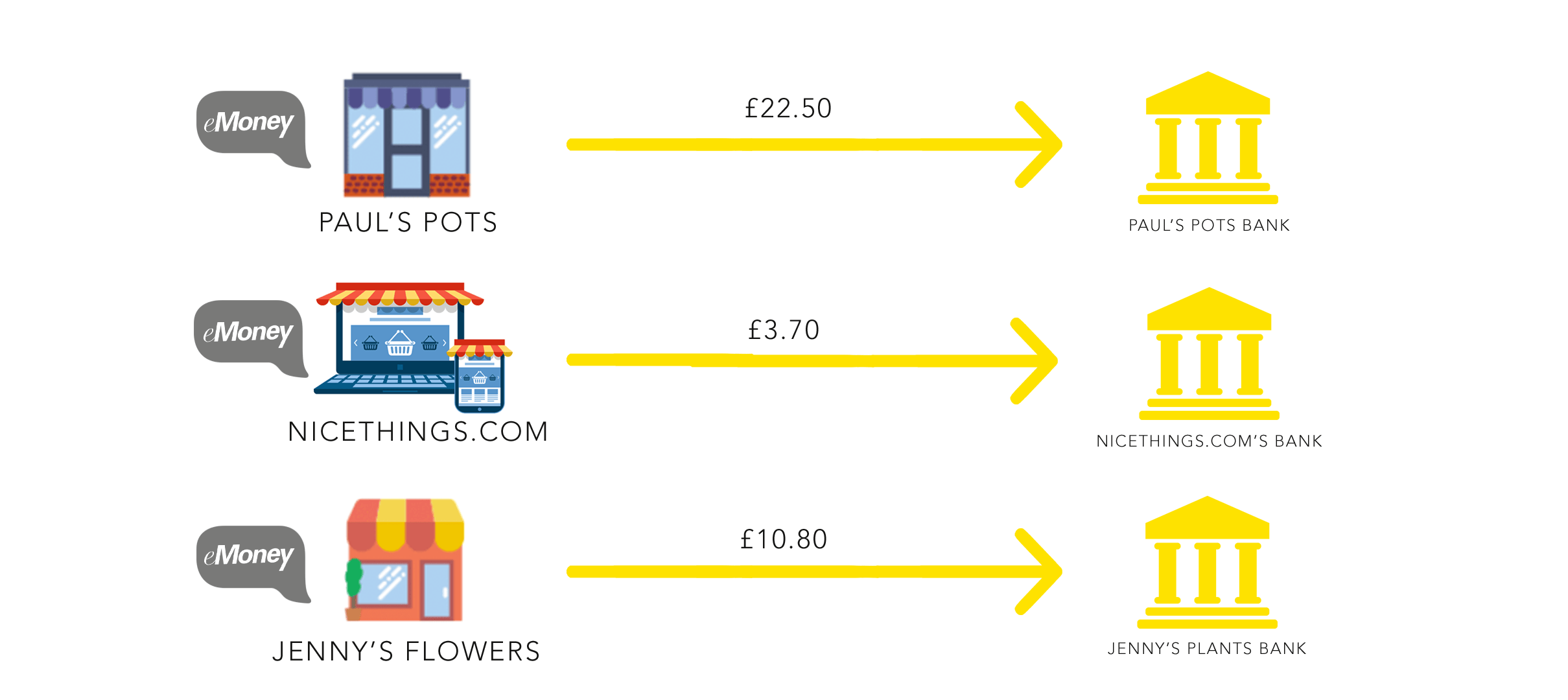

\n\nThis solution is difficult to scale. The more successful your business becomes, the more operational overhead is required to handle payments. Furthermore, if your platform has different fees for different sellers, this becomes even more complex.\n\nNot only this, but as of January 2018 firms acting in this way must become regulated as a financial institution. This is due to the regulatory changes of [PSD2](https://paybase.io/blog/psd2-what-is-it-will-it-affect-me), which aim to protect consumers and businesses by only allowing regulated institutions to handle client money.\n\n

\n \n

\n\nThe second method works differently. By using ‘electronic money’ (eMoney), payments can be split automatically. With eMoney, all funds are held in one central bank account, with balances being reflected on an electronic ledger. More info on this can be found in [this](https://paybase.io/blog/payment-gateways-vs-emoney) blog, but let’s look at how this works in practice.\n\nYou have a marketplace called ‘Nicethings.com’. A buyer goes on to your marketplace and decides to buy a pot from a particular seller (Paul’s Pots). The pot costs £25 and the buyer is happy with the price. You as the marketplace charge sellers 10% on any sales they make.\n\nThe buyer pays online by card, as with any online purchase. That £25 then goes to the central account. Due to the commission charge, £22.50 is displayed on the seller’s eMoney balance (Paul’s Pots), and £2.50 is displayed on your eMoney balance as the platform. When the seller chooses to withdraw their £22.50, it is debited from the central account and transferred to their bank account (again, automatically). When you as the platform choose to withdraw, the exact same thing happens.\n\nThe diagrams below explain how this payment flow looks. It works the exact same way for all merchants on your marketplace.\n\n\n\n\n\nAs you can see, this is a far easier and cleaner approach to platform payments. If a platform decides to use eMoney, they must either become regulated as an eMoney institution (a high-cost process which will take at least 6 months or possibly even years), or partner with a firm that is.\n\nPaybase was built to serve these businesses. The Paybase solution not only splits payments however a client wishes, but ensures they are covered in terms of all current and future regulatory standards.\n\nSo, whilst there are various ways in which payments can work for platform businesses, using eMoney is by far the most efficient option. If an eMoney solution is what your business needs, get in touch with us today by clicking [here](https://paybase.io/#get-in-touch).","excerpt":"\nChoosing the right payments option can be the best early decision your business makes\n\nIf you are currently setting up your platform and are starting to think about payments, bear in mind, platform payments work differently than payments for more tr...","cover":{"src":"https://paybase.imgix.net/blog/how-do-payments-work-hero-2.png","alt":"need one"},"link":{"to":"/blog/how-do-payments-work-for-online-marketplaces","copy":"Read more"},"tags":["Platform Economy","Payments","eMoney"]},{"id":"5611a978-eb24-5ab4-bcf4-2dc85ad5817a","title":"Payment Gateways vs eMoney – Everything you need to know","slug":"payment-gateways-vs-emoney","published":"2017-09-20T00:00:00.000Z","author":"Dan Whale","content":"\nYou may not be familiar with the term payment gateway, but you will have certainly used one. It is likely that you have used some form of eMoney as well, but what is the difference - and why does it matter?\n\n## Payment Gateway\nA payment gateway is what you use to make a card purchase online. Whether you’re buying a t-shirt, a holiday, pet insurance or your lunch, this is what you’ll use. You can think of it as the online equivalent of a card machine in a shop. It is an instrument that connects the merchant with your bank through an acquirer and the card schemes (more information on how the ‘four party model’ works can be found [here](https://www.visaeurope.com/about-us/four-party-model/)).\n\nPayment gateways allow merchants to hand the responsibility of the payment to third parties in place of requesting bank-to-bank transfers and are the only scalable way of taking card payments online. That being said, payment gateways are not always flawless. Handing the responsibility of the payment to a third party means that they can block payments they do not feel comfortable/secure with, which can result in bad customer experience. Furthermore the gateway page often takes the end user away from the product page or to a page that is branded differently. For some customers, this creates issues in terms of trust as they are asked to enter their card details into a screen they have not seen before.\n\nFinTechs such as Stripe have attempted to alleviate some of the drawbacks with payment gateways. Stripe have built an attractive payment gateway which sits well on any website, but what’s more impressive is how easy and transparent they have made their integration process for merchants. They were one of the first payments companies to openly display their API documentation on their website and they have made setting-up a payment gateway quick and simple.\n\nWhilst there are certain drawbacks to payment gateways, when it comes to supporting simple online payments (especially since the developments of FinTechs such as Stripe) they are more than adequate. However, what about when you need to support complex payments?\n\nThis is where eMoney comes in.\n\n## eMoney\nWith eMoney, everyone’s money balance is recorded on a ‘stored-value card’ or in an electronic account. Instead of the money being linked to individual bank accounts, all money is stored in an electronic ledger which reflects all eMoney accounts created. This allows for separate, private eMoney schemes to be built on eMoney infrastructure.\n\nFor example, eMoney is used for the Paybase-owned app Payfriendz. Users top-up their Payfriendz account, then money can be sent to, and between, other Payfriendz accounts and be withdrawn.\n\nThis is a lot more cost-effective as no money movement is actually involved in account to account transactions - it is only the balances of both parties that need to be adjusted in the ledger. What is more, the private eMoney scheme means that the company using it can set its own parameters, for instance around loyalty points and their conversion to fiat currency – of course, all within the regulatory framework.\n\nHowever, speaking more generally, eMoney opens the door to innovation through being a lightweight financial instrument. This is especially true for marketplaces. It permits possibilities such as multiple accounts for users, escrow accounts, loyalty accounts and multi currency accounts, all of which can be set up instantly. Let’s look at some examples:\n\n#### Marketplaces\nCurrently the majority of marketplaces use a standard payment gateway to accept their payments. This is not very practical. In this instance, all the payments that the marketplace receives need to, at some point, be reconciled and paid out to sometimes thousands of individual sellers.\n\nUsing eMoney, a customer can pay the seller’s account directly, whilst the marketplace can still easily take their cut. This eliminates the need for reconciliation and reduces operational overhead, allowing the marketplace to focus on their core business.\n\nMarketplaces aren’t just online stores with buyers and sellers such as Etsy, eBay, etc. Gig and sharing economy platforms are also marketplaces - marketplaces mainly focused on services. Giants such as Deliveroo and Uber are some of the main examples of this, however this is an industry that has [exploded](http://www.bbc.co.uk/news/uk-england-london-38248949) in recent years and now includes everything from freelance video producers to dog walkers.\n\neMoney infrastructure can help these types of platforms in the exact same way as it can help ‘standard’ marketplaces. Instead of money going to the platform to then be settled to each freelancer or supplier, it goes straight to the person who has performed the service/provided the good, with the platform automatically taking their cut.\n\nAnother great use case of eMoney in this context is escrow-like functionality. This would, for instance, allow a customer to pay a freelancer working for a handyman services platform to put up some shelves, with funds only being released when the shelves are up. This kind of payment system creates a lot more trust between the user and the service provider.\n\nFinally, eMoney infrastructure lends itself well to setting up loyalty programmes. If you are a marketplace, you could reward your sellers with loyalty points based on number and/or value of transactions they have. Due to the ease in which eMoney accounts can be created, a loyalty ‘points’ eMoney account can be opened for every merchant and the loyalty points periodically paid out in fiat currency.\n\n#### Issues with eMoney\nAs useful as eMoney can be, it isn’t the most straightforward thing to set-up and operate. Firstly, to operate as an eMoney Institution you must be authorised by the FCA - this is a long process. Even if eventually authorised, compliance and anti-money laundering (AML) procedures must be implemented, which can be arduous and costly.\n\nAdditionally, funds need to be held in a certain type of bank account called a ‘client segregated’ bank account. As with authorisation from the FCA, this account is not opened arbitrarily, especially due to FinTechs often being seen as higher risk. Finally, the level of tech required to build eMoney infrastructure is no small ask. Firms must integrate with multiple payments providers that use legacy technology, so no matter how impressive your technology is, it must be compatible with that of others.\n\n## Paybase\nWe started Paybase because we see the vast potential of eMoney yet are aware of how difficult it can be for companies to set up and implement eMoney infrastructure if payments aren’t their core focus. The Paybase Platform resolves the issues around eMoney described above by providing an end-to-end solution covering payments, compliance and risk. With no set-up fees or monthly minimums, we provide a cost-effective solution which gets your business to market quickly.\n\nOur single API and cutting edge technology allow for simple, rapid integration and unprecedented flexibility.\n\nIf you are a marketplace or an app that could benefit from eMoney infrastructure, get in touch!\n\n[Twitter](https://twitter.com/paybase) [LinkedIn](https://www.linkedin.com/company/paybase/)\n","excerpt":"\nYou may not be familiar with the term payment gateway, but you will have certainly used one. It is likely that you have used some form of eMoney as well, but what is the difference - and why does it matter?\n\nPayment Gateway\nA payment gateway is what...","cover":{"src":"https://paybase.imgix.net/blog/payment-gateway.jpg","alt":"need one"},"link":{"to":"/blog/payment-gateways-vs-emoney","copy":"Read more"},"tags":["Payments","eMoney","Marketplaces"]},{"id":"c6c5f34d-b2db-54ae-9a4c-7c56e9a5bc7c","title":"What to expect from the first Paybase Workshop","slug":"what-to-expect-from-the-first-paybase-workshop","published":"2018-10-04T00:00:00.000Z","author":"Dan Whale","content":"\nThe first #PaybaseWorkshop is fast approaching and we’re really looking forward to bringing together a lot of innovators in the platform business space. The event has now sold out, but if you weren’t able to get a ticket, we will be hosting many more like it in the near future. For the lucky ones that did get a ticket, here’s a little more information as to what to expect from the event. \n\n**Speakers**\n\nWe have 3 guest speakers for the workshop, each bringing a particular skill set and expertise that all working in platform businesses can benefit from. \n\n\n

\n \n

\n\n**Fayssal Loussaief - Lead Strategist at Brilliant Basics** \n\nBrilliant Basics has designed and created digital products and services for some of the world’s biggest companies. From HSBC to BT, its proficiency in UX has seen the company build products that are used by millions everyday.\n \nFayssal joined the company with a wealth of expertise. Having worked as the product development lead at Visa Europe and led the digital propositions of RBS and Natwest, Fayssal has gained a particular appreciation of customer experience and user experience within payments and finance. At the Paybase workshop, he will be talking about how your marketplace can build a payments option that is both UX and CX-focussed.\n \n

\n \n

\n\n**Garrett Cassidy - CEO and Co-Founder at Trezeo**\n\nTrezeo is removing a huge pain-point that exists in the gig economy. For platform business workers, or anyone that is self-employed, getting finances in order can be very stressful. Some weeks you are paid more than others and it can be hard to know where you stand in terms of bills. The Trezeo business account smooths out your income to allow you to get back to doing what you love. \n \nCEO and Co-Founder Garrett Cassidy’s 20 years experience in financial services enabled him to spot the difficulty that self-employed/gig economy workers were facing, and how to solve it. He built an award-winning startup which is increasingly relevant as working patterns are becoming more and more flexible. At the Paybase workshop, Garrett will be telling us the story of Trezeo, sharing invaluable wisdom on growing a business as well as how the users of your platform business can benefit from his fantastic service. \n \n

\n \n

\n\n**Sjoerd Handgraaf - CMO at Sharetribe**\n\nSharetribe is a business which simplifies the journey of creating a marketplace, making platform technology available to everyone. Its comprehensive yet customisable approach has helped many innovative platform businesses get to market and make profit within a very short time period.\n \nAs the company’s CMO for the past 2 years, Sjoerd has talked to hundreds of aspiring marketplace entrepreneurs. This has shown him the most common pitfalls, but also the most successful tactics and strategies in marketing marketplaces. Sjoerd will be sharing his expertise and engaging with the audience, offering direction on how you can best grow your business. This is an amazing opportunity to learn usable skills and techniques from a true industry expert.\n\n**Networking**\n\nThere will also be informal networking sessions with refreshments. This will give you the chance to discuss business challenges with the very people who are likely to have experienced them as well. We hope for this event to be the first step in establishing a community that can be drawn from for assistance and guidance. If nothing else, you’ll hear about some really interesting new businesses!\n\nWe are dedicated to hosting a helpful and relevant event that all our attendees can really benefit from. As such, we’ve created the following form to learn what stage of the business lifecycle our attendees are at, we’d really appreciate your input!\n\n \n\n\n[Twitter](https://twitter.com/paybase) [LinkedIn](https://www.linkedin.com/company/paybase/)\n","excerpt":"\nThe first #PaybaseWorkshop is fast approaching and we’re really looking forward to bringing together a lot of innovators in the platform business space. The event has now sold out, but if you weren’t able to get a ticket, we will be hosting many mor...","cover":{"src":"https://paybase.imgix.net/blog/paybase-workshop-hero-min.jpg","alt":"need one"},"link":{"to":"/blog/what-to-expect-from-the-first-paybase-workshop","copy":"Read more"},"tags":["Workshop","Platform Economy","Event"]}]}}}

\n

\n \n

\n \n

\n