{"componentChunkName":"component---src-templates-blogpost-tsx","path":"/blog/welcome-to-paybase","result":{"pageContext":{"isCreatedByStatefulCreatePages":false,"id":"0555452b-d9d7-517d-934f-6391ae4858c2","title":"Welcome to Paybase","slug":"welcome-to-paybase","published":"2017-05-16T00:00:00.000Z","author":"Ellie Fryer-Ambler","content":"\nToday, we’re excited to launch our new website and new brand all in the same month as moving our growing team to our new office in London Bridge.\n\n\n\n## Who are Paybase?\n\nFounded in 2013, we started out as a consumer-facing business and launched the money transfer app Payfriendz.\n\nWhen founding Payfriendz, the plan was to make our customers our core focus, listening to feedback and building a product loved by many... Things didn’t go according to plan. We were quickly sucked into the intricacies of providing an electronic money product, the regulatory and compliance requirements that came with it and the vast array of technical integrations we had to make. We searched for a secure, modern, tech-first payments partner who could deliver our requirements, but were instead drowned in work whilst trying to make do with legacy providers.\n\nThis is when we decided to build the Paybase Platform - a developer-native, end-to-end solution for payments, compliance, and risk.\n\nAlthough we still love the Payfriendz brand for our millennial targeted payment transfer app, we needed a name and brand to reflect our company's shift in focus to our Platform offering. Paybase is the perfect fit.\n\nUnlike traditional payment solutions, Paybase gives you the best of payments and technology-driven flexibility - all rolled into one unified API for quick and easy integration.\n\n## See how we compare\n\n**Without Paybase**\n\n\n\n**With Paybase**\n\n\n\n**Sounds good, but who is it for?**\n\nIt’s perfect for marketplaces such as crowdfunding sites or gig/sharing economy platforms or any app/product that requires payments infrastructure. [Find out more](/).\n\n> \"Our mission is to democratise access to payments infrastructure by removing the prohibitive cost and knowledge barriers so that our partners can focus on their core business.\"\n>\n> - Anna Tsyupko, CEO\n\n**What’s next?**\n\nOver the coming weeks and months, we’ll use this blog to introduce the team behind the Platform as well as give insights to some of the features and projects we’re working on.\n\nFeel free to contact us anytime using [hello@paybase.io](mailto:hello@paybase.io) or follow us on LinkedIn.\n","excerpt":"\nToday, we’re excited to launch our new website and new brand all in the same month as moving our growing team to our new office in London Bridge.\n\nWho are Paybase?\n\nFounded in 2013, we started out as a consumer-facing business and launched the money...","cover":{"src":"https://paybase.imgix.net/blog/welcome-to-paybase-hero.jpg","alt":"need one"},"link":{"to":"/blog/welcome-to-paybase","copy":"Read more"},"tags":["Paybase Platform","Payments","eMoney"],"related":[{"id":"61011136-46c8-59dc-9f67-5975d67939f3","title":"How do payments work for online marketplaces / gig / sharing economy platforms?","slug":"how-do-payments-work-for-online-marketplaces","published":"2019-02-27T00:00:00.000Z","author":"Dan Whale","content":"\n### Choosing the right payments option can be the best early decision your business makes\n\nIf you are currently setting up your platform and are starting to think about payments, bear in mind, platform payments work differently than payments for more traditional ecommerce businesses.\n\nFor traditional ecommerce businesses, the payment flow is simple. Money is transferred from a buyer to a seller using a payment gateway and acquirer. We won’t walk you through the entire ‘four-party model’ (as it is known) now, but if you’re interested in how it works, [this article](https://www.visaeurope.com/about-us/four-party-model/) explains it well. This is how online card payments have been made for decades, with the experience becoming sleeker and quicker for the customer in recent years.\n\nBut the payment flow of a platform business is different. Platform businesses do not usually sell their own products or services. Instead, they connect buyers and sellers and charge a commission on transactions between them. This means that payments need to be routed. This can be done in one of two ways.\n\nThe first method is to use a payment gateway and acquirer as traditional ecommerce businesses do. This entails taking in all payments from your buyers centrally, then calculating your commission, before finally manually transferring the remainder to each individual seller.\n\n

\n \n

\n\nThis solution is difficult to scale. The more successful your business becomes, the more operational overhead is required to handle payments. Furthermore, if your platform has different fees for different sellers, this becomes even more complex.\n\nNot only this, but as of January 2018 firms acting in this way must become regulated as a financial institution. This is due to the regulatory changes of [PSD2](https://paybase.io/blog/psd2-what-is-it-will-it-affect-me), which aim to protect consumers and businesses by only allowing regulated institutions to handle client money.\n\n

\n \n

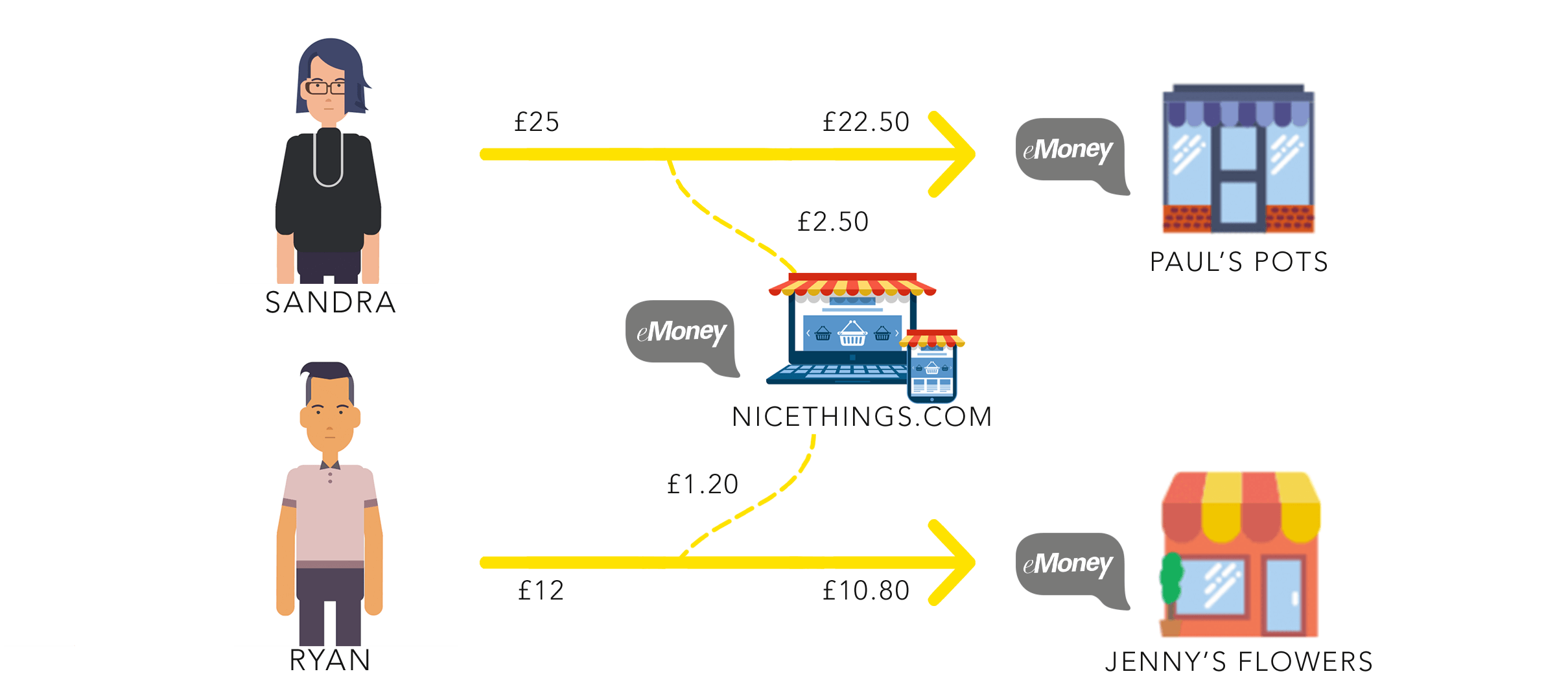

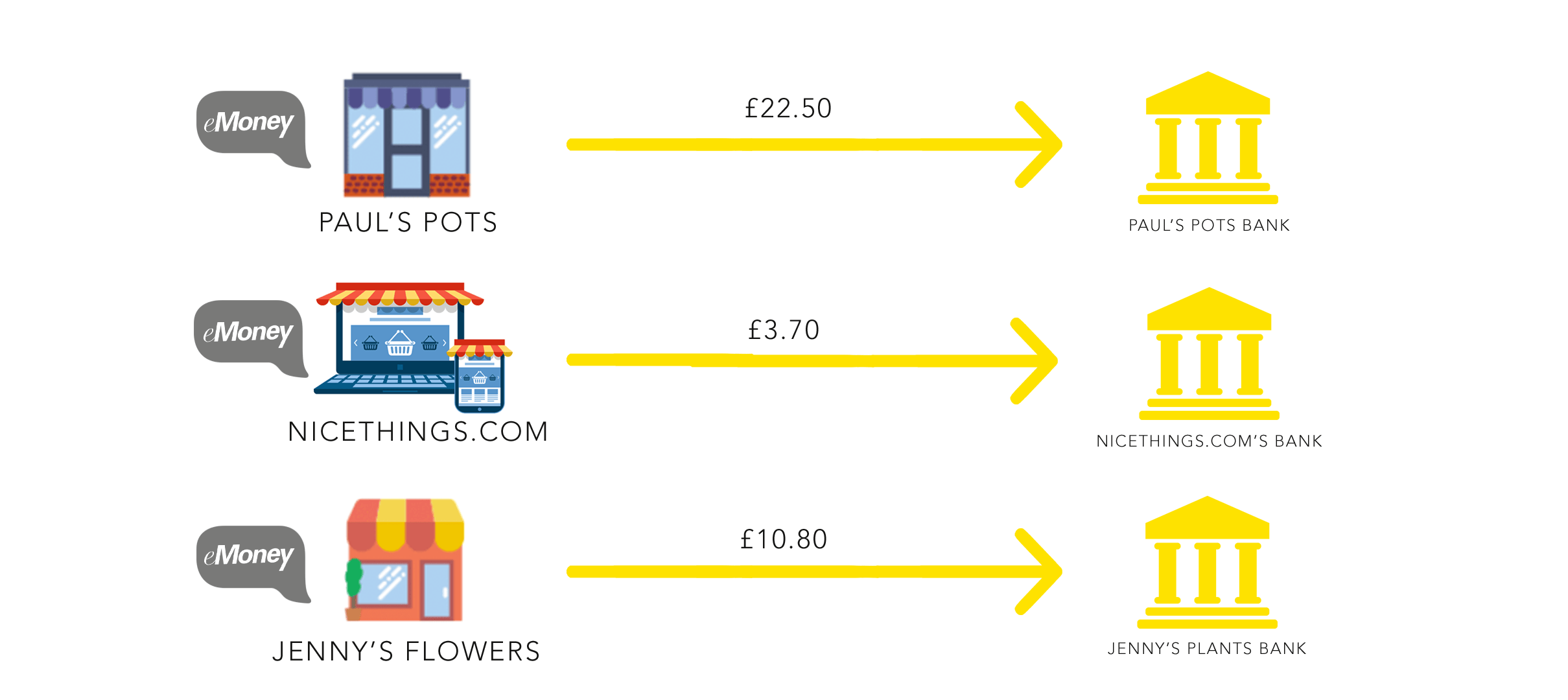

\n\nThe second method works differently. By using ‘electronic money’ (eMoney), payments can be split automatically. With eMoney, all funds are held in one central bank account, with balances being reflected on an electronic ledger. More info on this can be found in [this](https://paybase.io/blog/payment-gateways-vs-emoney) blog, but let’s look at how this works in practice.\n\nYou have a marketplace called ‘Nicethings.com’. A buyer goes on to your marketplace and decides to buy a pot from a particular seller (Paul’s Pots). The pot costs £25 and the buyer is happy with the price. You as the marketplace charge sellers 10% on any sales they make.\n\nThe buyer pays online by card, as with any online purchase. That £25 then goes to the central account. Due to the commission charge, £22.50 is displayed on the seller’s eMoney balance (Paul’s Pots), and £2.50 is displayed on your eMoney balance as the platform. When the seller chooses to withdraw their £22.50, it is debited from the central account and transferred to their bank account (again, automatically). When you as the platform choose to withdraw, the exact same thing happens.\n\nThe diagrams below explain how this payment flow looks. It works the exact same way for all merchants on your marketplace.\n\n\n\n\n\nAs you can see, this is a far easier and cleaner approach to platform payments. If a platform decides to use eMoney, they must either become regulated as an eMoney institution (a high-cost process which will take at least 6 months or possibly even years), or partner with a firm that is.\n\nPaybase was built to serve these businesses. The Paybase solution not only splits payments however a client wishes, but ensures they are covered in terms of all current and future regulatory standards.\n\nSo, whilst there are various ways in which payments can work for platform businesses, using eMoney is by far the most efficient option. If an eMoney solution is what your business needs, get in touch with us today by clicking [here](https://paybase.io/#get-in-touch).","excerpt":"\nChoosing the right payments option can be the best early decision your business makes\n\nIf you are currently setting up your platform and are starting to think about payments, bear in mind, platform payments work differently than payments for more tr...","cover":{"src":"https://paybase.imgix.net/blog/how-do-payments-work-hero-2.png","alt":"need one"},"link":{"to":"/blog/how-do-payments-work-for-online-marketplaces","copy":"Read more"},"tags":["Platform Economy","Payments","eMoney"]},{"id":"cc72e92f-c645-5463-84d2-aaf934b45e07","title":"Why eMoney is More Than Just Escrow","slug":"why-emoney-is-more-than-just-escrow","published":"2017-12-13T00:00:00.000Z","author":"Dan Whale","content":"\n### The escrow functionality of eMoney is massively useful, but there are many other exciting ways in which eMoney is being used.\n\nPut simply, eMoney is money recorded on a ‘stored-value card’ or in an electronic account. Instead of the money being linked to individual bank accounts, all funds are held in one single bank account, with an electronic ledger reflecting all eMoney accounts created. This means that transfers between eMoney accounts do not actually involve the movement of money, the ledger is simply adjusted. Not only this, but eMoney’s flexible nature means that accounts can be created quickly and easily.\n\nThis ledger-based, digitally focussed approach is well suited to features such as escrow. Escrow functionality allows for money to be placed into an account, but only transferred to another account once a certain condition is met. One of the most popular uses for this is crowdfunding, as it allows contributors to donate to a cause with the guarantee that their money will only be taken if the target is reached. So where does eMoney come in? The speed and flexibility of eMoney account creation works really well for escrow accounts as they need to be set up quickly and are almost always temporary. With eMoney, a crowdfunding project can exist for just a week or even just one day.\n\nHowever, this is not to suggest that escrow is eMoney’s only purpose. In fact, it’s not even its primary function. There are thousands of Electronic Money Institutions (EMIs) operating in the UK, all leveraging eMoney in different ways. Here are just a few examples of how eMoney is used in financial services today.\n\n## Prepaid cards\nOne of the main uses of eMoney is prepaid cards. Prepaid cards are topped-up from either a bank account or through physical cash. The cards differ from debit and credit cards as they are not linked to a bank account, meaning it is not usually possible to receive salary, set up direct debits or transfer to the bank accounts of others with prepaid cards. But being based on eMoney, these card accounts can be created very quickly and hold benefits in various contexts, such as corporate expenses, gifting, currency exchange and other innovative services. \n\n#### Corporate cards\nPrepaid cards allow businesses to offer their employees expenses cards, sparing the need for employees to use their own debit/credit card and then be reimbursed through the company. As well as avoiding the risk of spending more than what the budget allocates, the card can be shared between employees, with the accounting department handling the bookkeeping centrally.\n\n#### Gift cards\nOne of the most common uses of prepaid cards is for gifting. The gift card industry is worth over [£6bn](http://www.ukgcva.co.uk/) annually, with cards being given out as presents and corporate rewards. Giving people gift cards has the advantage of being a ‘forced treat’. A gift of £20 cash can go into the recipient’s bank account and end up going out as bills, but a £20 gift card makes them buy something for themselves. This scheme is also hugely beneficial for the store, as they are not only paid a rounded fee in advance, but the truth is that many gift cards go unused - [£300m](http://www.thisismoney.co.uk/money/bills/article-4097526/Got-gift-card-Christmas-Spend-join-300m-black-hole.html) a year is gained by merchants in unused gift cards.\n\n#### Currency cards\nCurrency cards are a type of prepaid card that allow people to purchase foreign currencies to use when they travel. The customer buys, for example, €500 at a fixed rate in GBP, which is then loaded onto a currency card. This enables customers to avoid heavy international transaction fees that occur when using a debit card abroad and feel more secure, not having €500 cash in their suitcase.\n\n#### Innovative services\n[Monzo](https://monzo.com/) has demonstrated how a good banking product can be initially built upon a prepaid system. Monzo links users’ transaction data to real-time spending reports, allowing users to keep track of their money and budget their spending based on automatic categorisation of purchases (eg. entertainment, travel, bills). Using a prepaid system allowed Monzo to get up and running as quickly as possible whilst they applied for their full banking licence. \n\nThese are only a few examples of prepaid card industries, but they demonstrate the variety and extent to which prepaid cards can be used. Originally introduced in the [1970s](http://blog.unibulmerchantservices.com/a-brief-history-of-prepaid-cards/), prepaid cards are arguably the most proven use of eMoney, and are certainly showing no signs of losing popularity.\n\n## Loyalty\nAnother excellent use of eMoney is loyalty. Because eMoney allows accounts to be created so quickly and easily, a business can comfortably set up a loyalty account alongside a customer’s account, paying into it as and when to reflect spending rewards. For example, for every 10th purchase a customer makes, the merchant could transfer £5 worth of ‘loyalty points’ to the customer’s account, which could then be used as credit for the store when the customer makes a subsequent transaction.\n\nIf a merchant partners with Paybase, this whole process can be more sophisticated. With our Logic Engine, transferring loyalty points based on transactions can not only be automated, but configured by the business itself. The merchant can decide how and when points are allocated for each customer or type of customer. As such, payments is not a rigid necessity to be shoehorned into a business model, but a tool which can actually increase business potential.\n\n## P2P and Group Payments\nAs mentioned earlier, when transactions are made between eMoney accounts, all that is required is an adjustment of the ledger. Because of this, eMoney accounts can easily transfer money between each other at high speed and low cost, without separate parties needing to know each other’s bank details. This allows users to make person-to-person (P2P) payments, instantly, on a variety of apps.\n\nUsing this same mechanism, apps and services are appearing which allow customers to pool their money onto one card, which can perhaps be used abroad - ideal for group holidays and stag/hen dos. Some apps facilitate group payments and bill splitting for housemates, all taken care of with a few clicks. When it comes to P2P and group payments, eMoney’s capabilities are solving genuine problems with a strong focus on UX.\n\n## Payment Routing\nFurthermore, another great use case of eMoney is payment routing. In recent years, commerce has changed. The growth of the sharing economy has seen companies like Uber and AirBnB dominate their markets and thousands more firms appear, all based around the concept of connecting buyers to independent suppliers. In the same way that the sharing economy has connected dog owners to dog walkers and homeowners to holiday-goers, it has also birthed scores of online marketplaces, allowing anyone to sell items from arts and crafts to clothing.\n\nWhat has been slower to change, however, is the payment processing. Many of these sharing economy platforms still take all payments centrally, which then have to be transferred manually to each supplier/merchant’s bank account, after the platform has taken their cut (which may be unique for each supplier/merchant). But an eMoney system allows customers to pay directly into a supplier’s/merchant’s eMoney account, removing the need for manual reconciliation. Using an eMoney solution, Paybase can offer its partners the ability to collect their fees automatically, even if they differ between individual merchants and suppliers. This reduces operational overhead for sharing economy platforms and marketplaces and allows them to concentrate on running their business.\n\n

\n \n

\n\n## In-app Payments\nFinally, eMoney is used to facilitate in-app payments between parties. There are many apps and services which connect different users or groups, but making payments has always been a pain-point as users must be taken outside of the app. eMoney can change this, and by introducing in-app payments companies can augment the value proposition of their product. One use case to examine would be EdTech.\n\nEdTech is an industry that has grown substantially in recent years, with apps dedicated to connecting schools and teachers to parents. What most EdTech products don’t solve, however, is the payment aspect of the school/parent interaction. Parents still need to put cash in an envelope and hand it to their child or use a different portal or system to make a payment for the school trip they’ve been informed about in the EdTech product. What eMoney can provide is a way for parents to pay for their child’s music lesson, after school club and school dinner directly in the EdTech product - it's simply a case of setting up separate eMoney accounts for the various parties.\n\nIn short, escrow is one great use case for eMoney, especially within the context of crowdfunding. However, we should not let that fact alter the perception of eMoney. Its impact on prepaid cards, loyalty systems, P2P payments, in-app payments and sharing economy platforms and marketplaces is simply too great to ignore.\n\nIf you think your business could benefit from an eMoney solution, please get in touch with us!\n\n[Twitter](https://twitter.com/paybase) [LinkedIn](https://www.linkedin.com/company/paybase/) \n","excerpt":"\nThe escrow functionality of eMoney is massively useful, but there are many other exciting ways in which eMoney is being used.\n\nPut simply, eMoney is money recorded on a ‘stored-value card’ or in an electronic account. Instead of the money being link...","cover":{"src":"https://paybase.imgix.net/blog/pound.jpg","alt":"need one"},"link":{"to":"/blog/why-emoney-is-more-than-just-escrow","copy":"Read more"},"tags":["Escrow","eMoney","Payments"]},{"id":"9efb11a0-ad48-5f77-b2cf-5cbd28795246","title":"Payment Gateways vs eMoney – Everything you need to know","slug":"payment-gateways-vs-emoney","published":"2017-09-20T00:00:00.000Z","author":"Dan Whale","content":"\nYou may not be familiar with the term payment gateway, but you will have certainly used one. It is likely that you have used some form of eMoney as well, but what is the difference - and why does it matter?\n\n## Payment Gateway\nA payment gateway is what you use to make a card purchase online. Whether you’re buying a t-shirt, a holiday, pet insurance or your lunch, this is what you’ll use. You can think of it as the online equivalent of a card machine in a shop. It is an instrument that connects the merchant with your bank through an acquirer and the card schemes (more information on how the ‘four party model’ works can be found [here](https://www.visaeurope.com/about-us/four-party-model/)).\n\nPayment gateways allow merchants to hand the responsibility of the payment to third parties in place of requesting bank-to-bank transfers and are the only scalable way of taking card payments online. That being said, payment gateways are not always flawless. Handing the responsibility of the payment to a third party means that they can block payments they do not feel comfortable/secure with, which can result in bad customer experience. Furthermore the gateway page often takes the end user away from the product page or to a page that is branded differently. For some customers, this creates issues in terms of trust as they are asked to enter their card details into a screen they have not seen before.\n\nFinTechs such as Stripe have attempted to alleviate some of the drawbacks with payment gateways. Stripe have built an attractive payment gateway which sits well on any website, but what’s more impressive is how easy and transparent they have made their integration process for merchants. They were one of the first payments companies to openly display their API documentation on their website and they have made setting-up a payment gateway quick and simple.\n\nWhilst there are certain drawbacks to payment gateways, when it comes to supporting simple online payments (especially since the developments of FinTechs such as Stripe) they are more than adequate. However, what about when you need to support complex payments?\n\nThis is where eMoney comes in.\n\n## eMoney\nWith eMoney, everyone’s money balance is recorded on a ‘stored-value card’ or in an electronic account. Instead of the money being linked to individual bank accounts, all money is stored in an electronic ledger which reflects all eMoney accounts created. This allows for separate, private eMoney schemes to be built on eMoney infrastructure.\n\nFor example, eMoney is used for the Paybase-owned app Payfriendz. Users top-up their Payfriendz account, then money can be sent to, and between, other Payfriendz accounts and be withdrawn.\n\nThis is a lot more cost-effective as no money movement is actually involved in account to account transactions - it is only the balances of both parties that need to be adjusted in the ledger. What is more, the private eMoney scheme means that the company using it can set its own parameters, for instance around loyalty points and their conversion to fiat currency – of course, all within the regulatory framework.\n\nHowever, speaking more generally, eMoney opens the door to innovation through being a lightweight financial instrument. This is especially true for marketplaces. It permits possibilities such as multiple accounts for users, escrow accounts, loyalty accounts and multi currency accounts, all of which can be set up instantly. Let’s look at some examples:\n\n#### Marketplaces\nCurrently the majority of marketplaces use a standard payment gateway to accept their payments. This is not very practical. In this instance, all the payments that the marketplace receives need to, at some point, be reconciled and paid out to sometimes thousands of individual sellers.\n\nUsing eMoney, a customer can pay the seller’s account directly, whilst the marketplace can still easily take their cut. This eliminates the need for reconciliation and reduces operational overhead, allowing the marketplace to focus on their core business.\n\nMarketplaces aren’t just online stores with buyers and sellers such as Etsy, eBay, etc. Gig and sharing economy platforms are also marketplaces - marketplaces mainly focused on services. Giants such as Deliveroo and Uber are some of the main examples of this, however this is an industry that has [exploded](http://www.bbc.co.uk/news/uk-england-london-38248949) in recent years and now includes everything from freelance video producers to dog walkers.\n\neMoney infrastructure can help these types of platforms in the exact same way as it can help ‘standard’ marketplaces. Instead of money going to the platform to then be settled to each freelancer or supplier, it goes straight to the person who has performed the service/provided the good, with the platform automatically taking their cut.\n\nAnother great use case of eMoney in this context is escrow-like functionality. This would, for instance, allow a customer to pay a freelancer working for a handyman services platform to put up some shelves, with funds only being released when the shelves are up. This kind of payment system creates a lot more trust between the user and the service provider.\n\nFinally, eMoney infrastructure lends itself well to setting up loyalty programmes. If you are a marketplace, you could reward your sellers with loyalty points based on number and/or value of transactions they have. Due to the ease in which eMoney accounts can be created, a loyalty ‘points’ eMoney account can be opened for every merchant and the loyalty points periodically paid out in fiat currency.\n\n#### Issues with eMoney\nAs useful as eMoney can be, it isn’t the most straightforward thing to set-up and operate. Firstly, to operate as an eMoney Institution you must be authorised by the FCA - this is a long process. Even if eventually authorised, compliance and anti-money laundering (AML) procedures must be implemented, which can be arduous and costly.\n\nAdditionally, funds need to be held in a certain type of bank account called a ‘client segregated’ bank account. As with authorisation from the FCA, this account is not opened arbitrarily, especially due to FinTechs often being seen as higher risk. Finally, the level of tech required to build eMoney infrastructure is no small ask. Firms must integrate with multiple payments providers that use legacy technology, so no matter how impressive your technology is, it must be compatible with that of others.\n\n## Paybase\nWe started Paybase because we see the vast potential of eMoney yet are aware of how difficult it can be for companies to set up and implement eMoney infrastructure if payments aren’t their core focus. The Paybase Platform resolves the issues around eMoney described above by providing an end-to-end solution covering payments, compliance and risk. With no set-up fees or monthly minimums, we provide a cost-effective solution which gets your business to market quickly.\n\nOur single API and cutting edge technology allow for simple, rapid integration and unprecedented flexibility.\n\nIf you are a marketplace or an app that could benefit from eMoney infrastructure, get in touch!\n\n[Twitter](https://twitter.com/paybase) [LinkedIn](https://www.linkedin.com/company/paybase/)\n","excerpt":"\nYou may not be familiar with the term payment gateway, but you will have certainly used one. It is likely that you have used some form of eMoney as well, but what is the difference - and why does it matter?\n\nPayment Gateway\nA payment gateway is what...","cover":{"src":"https://paybase.imgix.net/blog/payment-gateway.jpg","alt":"need one"},"link":{"to":"/blog/payment-gateways-vs-emoney","copy":"Read more"},"tags":["Payments","eMoney","Marketplaces"]}]}}}

\n

\n